In most cases, detailed transactions are recorded directly in these general ledger accounts. In the latter case, a person researching an issue in the financial statements must refer back to the subsidiary ledger to find information about the original transaction.

General Ledger vs Sub Ledger

For large scale businesses where many transactions are conducted, it may not be convenient to enter all transactions in the general ledger due to the high volume. In such cases, individual transactions are recorded in ‘subsidiary ledgers’, and the totals are transferred to an account in the general ledger. This account is referred to as the ‘Control account’, and account types that generally have a high activity level is recorded here.

The subsidiary ledgers are now part of the double entry system, and to extract a trial balance it would be necessary to collect information on the balances from each of the ledgers. In order to avoid this situation, control accounts are maintained in the general ledger for each of the subsidiary ledgers. A subsidiary ledger stores the details for a general ledger control account.

A subsidiary ledger contains the details to support a general ledger control account. For instance, the subsidiary ledger for accounts receivable contains the information for each of the company’s credit sales to customers, each customer’s remittance, return of merchandise, discounts, and so on. With these details in the subsidiary ledger, the Accounts Receivable account in the general ledger can report summary amounts for the accounts receivable activity. The accounts payable subsidiary ledger is similar to other subsidiary ledgers in that it merely provides details of the control account in the general ledger.

The company uses the periodic method of accounting for inventory. The GL is a set of master accounts and transactions are recorded and SL is an intermediary set of accounts linked to the general ledger. GL contains all debit and credit entries of transactions and entry for the same is done. Sub-ledger is a detailed subset of accounts that contains transaction information. Examples of the Subsidiary ledger are customer accounts, vendor accounts, bank accounts, and fixed assets.

A journal entry is usually recorded in the general ledger; alternatively, it may be recorded in a subsidiary ledger that is then summarized and rolled forward into the general ledger. The general ledger is then used to create financial statements for the business. A subsidiary account is an account that is kept within a subsidiary ledger, which in turn summarizes into a control account in the general ledger. A subsidiary account is used to track information at a very detailed level for certain types of transactions, such as accounts receivable and accounts payable. B. Enter the transactions into QuickBooks, complete all of the steps in the accounting cycle, and generate the same reports (journals trial balances, ledgers, financial statements).

Since bookkeeping using ledgers is older than the United States, it was an ingenious way to double-check without having to actually do everything twice. Today, computerized accounting information systems use the same method to store and total amounts, but it takes a lot less time. Sub-ledger is an intermediary set of accounts linked to the general ledger. It is a detailed subset of accounts that contains transaction information.

The total of sub-ledger should always match with the line item amount on the general ledger. So, it contains detail information regarding the business transaction and financial accounts. It can include purchase, payable, receivable, production cost and payroll. Recording of financial information is books of account as per standard accounting principle. The accounts receivable subsidiary ledger is essential to most businesses.

But the accounts receivable subsidiary ledger provides quick access to each customer’s balance and account activity. When the financial statements are prepared, the accounts payable total is listed with other short-term financial obligations under the current liabilities section of the balance sheet. The accounts payable subsidiary ledger is a breakdown of the total amount of payables listed on the general ledger.

The general ledger is usually printed and stored in an organization’s year-end book, which serves as the annual archive of its business transactions. A general ledger is the master set of accounts that summarize all transactions occurring within an entity.

Once information has been recorded in a subsidiary ledger, it is periodically summarized and posted to a control account in the general ledger, which in turn is used to construct the financial statements of a company. Most accounts in the general ledger are not control accounts; instead, individual transactions are recorded directly into them. Subsidiary ledgers are used when there is a large amount of transaction information that would clutter up the general ledger.

This situation typically arises in companies with significant sales volume. Thus, there is no need for a subsidiary ledger in a small company. The general ledger is comprised of all the individual accounts needed to record the assets, liabilities, equity, revenue, expense, gain, and loss transactions of a business.

- In a small business the accounts can be kept in one accounting general ledger and a trial balance can be extracted from that ledger.

While manually completed earlier, many companies use automated accounting packages that require minimum human intervention to prepare financial accounts at present. This is time-saving and reduces the possibility of human errors.

In other words, the subsidiary ledger contains the individual payables owed to each of the suppliers and vendors, as well as the amounts owed. The general ledger is a master ledger containing a summary of all the accounts that a company uses in operating its business. The subsidiary ledgers roll up to the general ledger, which records the aggregate totals of the subsidiary ledgers. The general ledger, in turn, allocates these totals into assets, liabilities, and equity accounts. Within most accounting systems, the process is performed via accounting software.

The subsidiary accounts receivable and payable ledgers have only one sided entries and therefore do not self balance. As only a section of the accounting system is self balancing such a system if sometimes referred to as a sectional balancing system.

There may be a subsidiary set of ledgers that summarize into the general ledger. An accounts payable subsidiary ledger is an accounting ledger that shows the transaction history and amounts owed to each supplier and vendor. An accounts payable (AP) is essentially an extension of credit from a supplier that gives a business (the buyer in the transaction) time to pay for the supplies. The subsidiary ledger records all of the accounts payables that a company owes. Recording financial information is a lengthy and time-consuming process, and its end result is the preparation of year-end financial statements.

What is the difference between subsidiary ledger and general ledger?

A subsidiary ledger contains the details to support a general ledger control account. For instance, the subsidiary ledger for accounts receivable contains the information for each of the company’s credit sales to customers, each customer’s remittance, return of merchandise, discounts, and so on.

In a small business the accounts can be kept in one accounting general ledger and a trial balance can be extracted from that ledger. In a larger business, where the transactions are too many to be managed by one person, subsidiary ledgers such as the accounts receivable ledger (sales ledger) and the accounts payable ledger (purchase ledger) will be opened.

Sub-ledger is part of the general ledger but the Trial balance is not prepared by using a general ledger. Ledger helps in the understanding of the financial of business and helps in the analysis of transactions.

Total and rule (draw a line under the column of numbers) the journals. Post the transactions to the subsidiary ledger and (using T-accounts) to the general ledger accounts. (Figure)Brown Inc. records purchases in a purchases journal and purchase returns in the general journal. Record the following transactions using a purchases journal, a general journal, and an accounts payable subsidiary ledger.

Accounting Principles I

What is the use of subsidiary ledger?

A subsidiary ledger is a group of similar accounts whose combined balances equal the balance in a specific general ledger account. The general ledger account that summarizes a subsidiary ledger’s account balances is called a control account or master account.

In contrast an accounting system in which all ledgers are individually balanced is referred to as a self balancing system. Also referred to as ‘subsidiary ledger’, this is a detailed subset of accounts that contains transaction information.

A business conducts many transactions within an accounting year, and these should be recorded in different accounts according to corresponding accounting standards. General ledger and sub ledger are such accounts that record business transactions. The relationship between these two is that multiple sub ledgers are attached to the general ledger. The use of accounts receivable and accounts payable control accounts creates an accounting system where only the general ledger is self balancing.

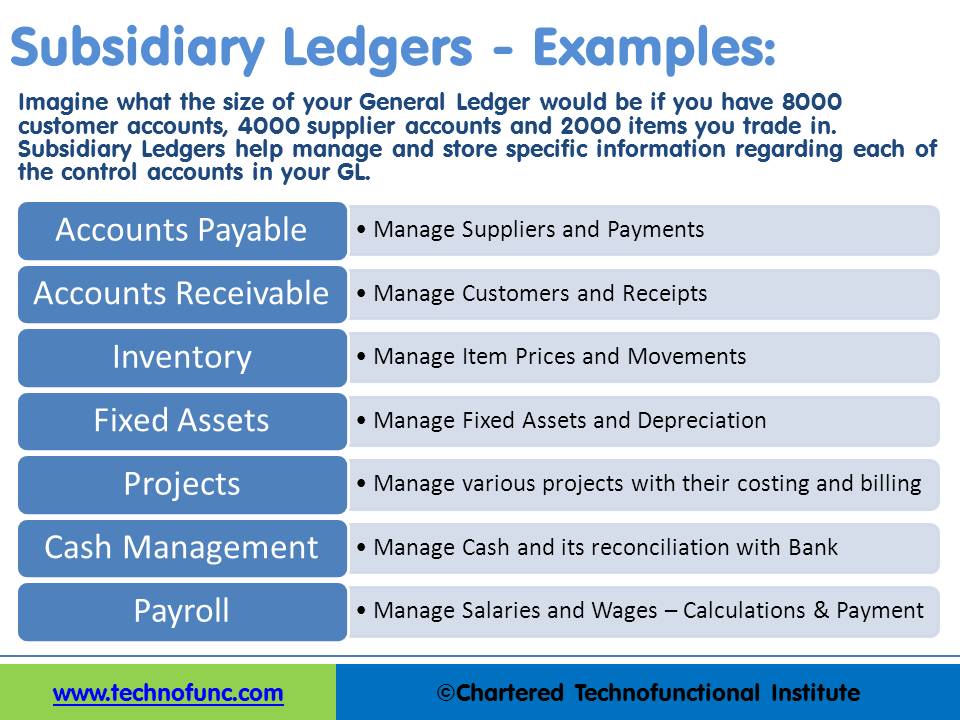

Examples of Subsidiary Ledgers

Subsidiary ledgers can include purchases, payables, receivables, production cost, payroll and any other account type. Since the total of the accounts receivable subsidiary ledger must agree with the balance shown in the accounts receivable general ledger account, the system helps us find mistakes.

E.g. ABC is a company which does around 75% of their sales on credit; as a result, it has many accounts receivables. The word “control” and its derivatives (subsidiary and parent) may have different meanings in different contexts. These concepts may have different meanings in various areas of law (e.g. corporate law, competition law, capital markets law) or in accounting. A journal entry is used to record a business transaction in the accounting records of a business.