Your bank may close your account

When you open up a bank account, financial institutions always outline their policies about deposits, including hold times for check deposits. Banks place these holds on checks in order to ensure the funds are available in the payer’s account before giving you access to the cash.

By doing this, they help you avoid incurring any charges—especially if you use the funds right away. You’re responsible for any checks you deposit, so you’ll have to repay any funds you use if the check bounces after you’ve taken the money.

It usually takes about two business days for a deposited check to clear, but it can take a little longer—about five business days—for the bank to receive the funds. How long it takes a check to clear depends on the amount of the check, your relationship with the bank, and the standing of the payer’s account.

It bears mentioning again that large deposits may come with a longer hold time. Some banks may hold checks that total $1,500 or higher for as many as 10 days. The number of days the bank holds these checks depends on your relationship with the institution. You’re more likely to get the money immediately—or within fewer than 10 days—if you have a healthy account balance and no history of overdrafts.

Civil penalties apply in all cases, with a common penalty amount equivalent to the face value of the check, a multiple of the check amount with a cap, or the check amount plus court and attorney fees. Overdraft protection is a fund transfer or loan that banks offer to customers to cover checks or debits larger than their account balances, so as to avoid nonsufficient funds fees. Banks often charge NSF fees when a presented payment is returned due to insufficient funds. A similar fee may be assessed when honoring payments from accounts with insufficient balances. The latter scenario describes an account overdraft (OD), which is often confused or used interchangeably with non-sufficient funds.

Banks originally sent physical checks to each other, but they increasingly use images of checks for improved efficiency. Assuming funds are available and there is no problem with the check, the paying bank transfers money to the receiving bank. If your bank tells you that you’ve cashed a bad check from a third party, contact the issuer of the check and try to resolve the problem and obtain payment.

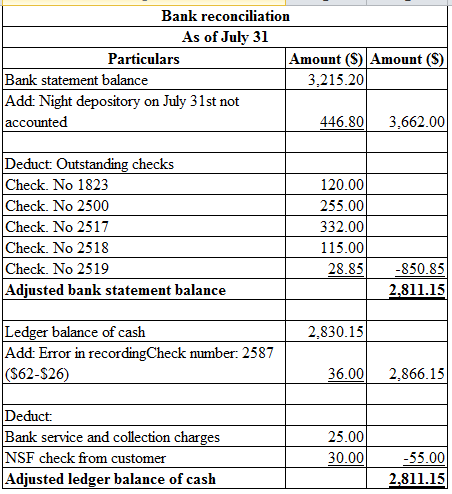

How to enter a bounced check using a journal entry

Managing your finances in an age where we have multiple bank accounts, checks, debit and credit cards can be complex. If you have multiple accounts or multiple cardholders on your accounts, you may not have good tabs on what is going on with your finances. We’ve all made mistakes and bounced checks, often through no fault of our own. Most of the time, simply covering the bounced check amount along with some fees will absolve you of your damages.

Accounts that have no or little history may automatically qualify for holds on all check deposits until the time that the bank feels you have solidified your relationship with it. Accounts that have negative history—that is, accounts that frequently bounce payments or go into overdraft—may also have checks held. If you don’t have sufficient money in your account, you may be subject to overdraft fees or low balance fees. If the bank believes you’ve committed fraud intentionally, it may close your account in addition to charging the fees.

However, some people write bad checks on purpose and those people can be criminally prosecuted. Writing checks you know will bounce, with the intent to defraud the merchant you are paying, can result in criminal charges being pressed against you.

Colloquially, NSF checks are known as “bounced” or “bad” checks. If a bank receives a check written on an account with insufficient funds, the bank can refuse payment and charge the account holder an NSF fee. Additionally, a penalty or fee may be charged by the merchant for the returned check. By law, certified checks and cashiers checks must be made available to you within one business day of deposit.

- The bank normally adds a nonsufficient funds (NSF) charge to your account, which can be as high as $35 for each bad check written.

- Bad checks are often written inadvertently by people who are simply unaware that their bank balances were too low.

Bad checks are often written inadvertently by people who are simply unaware that their bank balances were too low. Banks and vendors frequently charge fees for bounced checks, sometimes exceeding the amount for which the check was written. The bank normally adds a nonsufficient funds (NSF) charge to your account, which can be as high as $35 for each bad check written. You may also be on the hook for any charges the payee incurs as a result of your bad check.

Step 1: Record the bounced check in a journal entry

Wait a few days before contacting your bank about holds on deposited checks. A bad check is a check cashed when the person who wrote it doesn’t have adequate funds in their account to cover the check amount by the time it clears. Sometimes called a bounced check, but officially an NSF (nonsufficient funds) check, a bad check will be returned to you by the bank. An NSF check is a check that was not honored by the bank of the person or company writing the check because that account did not have a sufficient balance. As a result, the check is returned without being honored or paid.

The amount charged will be the amount of the check plus a bank fee. Penalties for people who tender checks knowing there are insufficient funds in their accounts vary by state.

AccountingTools

The intent is a very important component of this criminal charge; if you accidentally wrote a bad check, you will not be charged criminally. As with many criminal charges, writing bad checks, also called check fraud, can result in jail time.

What is a bounced check?

What happens when you have a NSF check?

An NSF check is a check that was not honored by the bank of the entity issuing the check, on the grounds that the entity’s bank account does not contain sufficient funds. This situation may also arise when a bank account has been closed. NSF is an acronym for “not sufficient funds.”

A history of overdrafts and low account balances may mean you’ll have to wait the full 10 days to receive the money. Imagine, for example, that you have $100 in your checking account and initiate an automated clearing house (ACH) or electronic check payment for a purchase in the amount of $120. If your bank refuses to pay the check, you incur an NSF fee and face any penalties or charges the seller assesses for returned checks. If the bank accepts the check and pays the seller, your checking account balance falls to $-20 and incurs an overdraft fee. Either way, the fee assessed by the bank reduces the available account balance.

Federal law (Regulation CC) requires that banksmake at least part of your deposit availableto you within a few days. For many items, like personal checks, the first $200 is available within one business day (if not immediately), and the remainder becomes available a few days later. Banks make larger amounts available for other items, such as government-issued checks, cashier’s checks, and USPS money orders. Logistically, the receiving bank or credit union (where the payee deposits or cashes the check) sends the check to the bank that the funds are drawn on, or to a clearinghouse.

But in the majority of states, the crime is considered a misdemeanor. If the check amount exceeds certain thresholds, the crime may be treated as a felony.