Engineering management must make this decision based on the cost of the products they are likely to procure, the importance of the bidders’ product to production, and other factors. When a business purchases capital assets, the Internal Revenue Service (IRS) considers the purchase a capital expense. In most cases, businesses can deduct expenses incurred during a tax year from their revenue collected during the same tax year, and report the difference as their business income. However, most capital expenses cannot be claimed in the year of purchase, but instead must be capitalized as an asset and written off to expense incrementally over a number of years.

Engineering would also inspect sample products to determine if the company or organisation can produce products they need. If the bidder passes both of these stages engineering may decide to do some testing on the materials to further verify quality standards. These tests can be expensive and involve significant time of multiple technicians and engineers.

Often purchasing managers research potential bidders obtaining information on the organizations and products from media sources and their own industry contacts. Additionally, purchasing might send Request for Information (RFI) to potential suppliers to help gather information.

This is the process where the organization identifies potential suppliers for specified supplies, services or equipment. These suppliers’ credentials and history are analyzed, with the products or services they offer. The bidder selection process varies from organization to organization, but can include running credit reports, interviewing management, testing products, and touring facilities. This process is not always done in order of importance, but rather in order of expense.

If another company buys the same computer to sell, it is considered inventory. Another method of decreasing administrative costs associated with repetitive contracts for common material, is the use of company credit cards, also known as “Purchasing Cards” or simply “P-Cards”. P-card programs vary, but all of them have internal checks and audits to ensure appropriate use. Purchasing managers realized once contracts for the low dollar value consumables are in place, procurement can take a smaller role in the operation and use of the contracts. There is still oversight in the forms of audits and monthly statement reviews, but most of their time is now available to negotiate major purchases and setting up of other long term contracts.

The formal bid process starts as low as $10,000 or as high as $100,000 depending on the organization. The bid usually involves a specific form the bidder fills out and must be returned by a specified deadline. Depending of the commodity being purchased and the organization the bid may specify a weighted evaluation criterion.

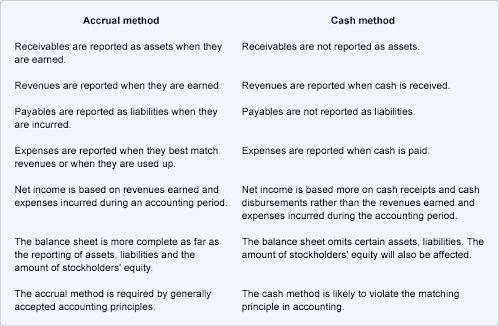

Is there a difference between the accounts Purchases and Inventory?

This means it ensures the supply of goods, production materials and equipment so that a smooth production and sales process can take place. For this, goods must be procured at the right time, in the right quantity, and of the right quantity. If the purchasing process falls down, there’s a risk that the business will not be able to manufacture products or keep the shelves stocked with sufficient volume to meet customer demand. Expense is a cost whose utility has been used up; it has been consumed.

purchases definition

Acquisitions under a specified dollar amount can be “user discretion” permitting the request or to choose who ever they want. This level can be as low as $100 or as high as $10,000 depending on the organization.

In the second case, converting from an asset to an expense is achieved with a debit to the cost of goods sold and a credit to the inventory account. Thus, in both cases, we have converted a cost that was treated as an asset into an expense as the underlying asset was consumed. The automobile asset is being consumed gradually, so we are using depreciation to eventually convert it to expense.

Capital expenses include the purchase of fixed assets, such as new buildings or business equipment, upgrades to existing facilities, and the acquisition of intangible assets, such as patents. Capital assets are significant pieces of property such as homes, cars, investment properties, stocks, bonds, and even collectibles or art. For businesses, a capital asset is an asset with a useful life longer than a year that is not intended for sale in the regular course of the business’s operation. For example, if one company buys a computer to use in its office, the computer is a capital asset.

- Using depreciation, a business expenses a portion of the asset’s value over each year of its useful life, instead of allocating the entire expense to the year in which the asset is purchased.

What are purchases accounting?

purchases definition. A temporary account used in the periodic inventory system to record the purchases of merchandise for resale. This account reports the gross amount of purchases of merchandise. Net purchases is the amount of purchases minus purchases returns, purchases allowances, and purchases discounts.

Other bids would be evaluated at the discretion of purchasing or the end users. Other bids may be evaluated by the end user or the buyer in Purchasing. Especially in small, private firms the bidders could be evaluated on criteria or factors that have little if anything to do with the actual bid. Examples of these factors are history of the bidder with the company, history of the bidder with the company’s senior management at other firms, and bidder’s breadth of products. All businesses need specific goods, materials and equipment to manufacture products, offer goods for sale to customers, or perform the services they are selling.

The asset is then depreciated over the total life of the asset, with a period depreciation expense charged to the company’s income statement, normally monthly. Accumulated depreciation is recorded on the company’s balance sheet as the summation of all depreciation expenses, and it reduces the value of the asset over the life of that asset. Operating expenses are expenses incurred during regular business, such as general and administrative expenses, research and development, and the cost of goods sold. Operating expenses are much easier to understand conceptually than capital expenses since they are part of the day-to-day operations. All operating expenses are recorded on a company’s income statement as expenses in the period when they were incurred.

Do purchases go on a balance sheet?

Someone has to ensure that these goods are bought into the company, in the right volume and at the right time, to meet the company’s requirements. Company B’s brand-new research facility, for instance, would be a capital expenditure. The costs of running the machinery in it, on the other hand, would be revenue expenditures.

These two types of expenses are treated differently when it comes to accounting and financial statements. However, a company can sometimes choose whether an expense will be an operating or capital expense, for example, whether a needed asset is leased or bought.

Purchasing topics

Examples of capital expenses include the purchase of fixed assets, such as new buildings or business equipment, upgrades to existing facilities, and the acquisition of intangible assets, such as patents. Essentially, a capital expenditure represents an investment in the business. Capital expenses are recorded as assets on a company’s balance sheet rather than as expenses on the income statement.

Are the goods purchased by a retailer an expense or an asset?

Using depreciation, a business expenses a portion of the asset’s value over each year of its useful life, instead of allocating the entire expense to the year in which the asset is purchased. This means that each year that the equipment or machinery is put to use, the cost associated with using up the asset is recorded. The rate at which a company chooses to depreciate its assets may result in a book value that differs from the current market value of the assets.

The rationale is the savings realized by processing these request the same as expensive items is minimal and does not justify the time and expense. Purchasing departments watch for abuses of the user discretion privilege. Acquisitions in a mid range can be processed with a slightly more formal process. This process may involve the user providing quotes from three separate suppliers.