As a result, it is very common that the amount of income taxes payable to governments in the near future differs from the income taxes expense reported on a company’s income statement. Once again, remember how income tax payments could be postponed by using accelerated depreciation for tax purposes?

A temporary difference is the difference between the asset or liability provided on the tax return (tax basis) and its carrying (book) amount in the financial statements. This difference will result in a taxable or deductible amount in the future.

Also referred to as taxes payable, this account documents the creation of a liability that is not yet paid to tax authorities. Accounting principles state that companies need to record the creation of the tax expense as it’s incurred, even though the money may not be payable in that same time period. Since income taxes are typically paid on a quarterly basis but reported annually, income taxes payable is classified as a current liability. Companies record both income tax expense and income tax payable in journal entries. For companies that use the cash basis for both financial and tax reporting, income tax expense equals income tax payable, the actual amount of tax to be paid.

Your company reports the expense of $10,000 and denotes $12,000 as tax payable. The financial accounting term income taxes payable is used to describe money owed to government authorities but not yet paid. Income taxes payable appears in the current liabilities section of the company’s balance sheet. The company’s resources (assets) increased because the company received $1,050 of promises (accounts receivable) from customers.

What are some examples of current liabilities?

It is important to note that while the company’s resources increased by $1,050, only $1,000 belongs to the company. The other $50 is owed to the state and, thus, appears as the current liability, sales taxes payable. This $50 is a result of the company acting as a revenue collection agency for the government.

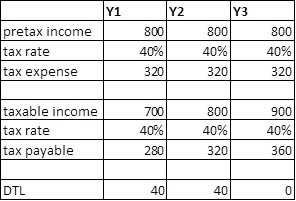

If the amount of income taxes payable must be paid within 12 months, it is classified as a current liability called income taxes payable. If the amount of income taxes does not have to be paid within 12 months, it is classified as a long-term liability called deferred income taxes payable. Deferred taxes payable are dollar amounts owed to governments for income taxes to be paid in the future. Deferred taxes payable arise when a company’s income taxes expense reported on its income statement differs from the amount of income taxes reported on its tax return. Such differences arise when a company uses methods in its accounting system that differ from those methods used in its taxes calculations.

Finally, deferred tax assets (like any other asset) need to be assessed for recoverability. Any amounts not deemed to be recoverable should be written off through expense. The current income tax payable or receivable is recorded with the offset to the P&L (current tax expense). Deferred tax assets and liabilities are normally recorded with the offsetting entry to the P&L (deferred tax expense). U.S. GAAP, specifically ASC Topic 740, Income Taxes, requires income taxes to be accounted for by the asset/liability method.

Income taxes payable are liabilities resulting from companies having more revenues than expenses. In addition to federal income taxes, many states also levy income taxes, although the rates vary from state to state. The actual income tax rates, both federal and state, are determined by tax authorities and are provided to companies for their use. Because the rates may change and their application can be quite complicated, companies use tax experts to calculate the amount of the taxes.

- Income taxes payable are liabilities resulting from companies having more revenues than expenses.

Income Tax Payable Definition

The company would report an income taxes payable current liability of $1,225,000 and a deferred income taxes payable long-term liability of $175,000 ($1,400,000 – $1,225,000). Remember, both the straight-line and accelerated depreciation methods result in the same total amounts of depreciation expense over an asset’s life. It is only the amounts of depreciation expense reported in each specific year that may differ. As a result, since the total depreciation expenses are the same over the asset’s life, the total income taxes expense will be the same. On the other hand, say your company calculates its income tax expense at $10,000, but its actual tax bill is $12,000.

$1,225,000 is a current liability, income taxes payable, because it will have to be paid within the next 12 months. $175,000 is a long-term liability, deferred income taxes payable, because it will not have to be paid within the next 12 months. Stockholders’ equity decreases by the full $1,400,000 of government services used up by management. Companies first need to calculate their current income taxes payable or receivable, then figure out their deferred tax assets and liabilities. The calculation of deferred tax assets and liabilities should be based on enacted tax law, not future expectations/assumptions.

However, a difference exists between income tax expense and income tax payable if companies use the accrual basis for financial reporting and the cash basis for tax filing. The difference is either a deferred tax liability or a deferred tax asset.

The company’s liabilities increased because $50 of the accounts receivable do not belong to the company, but are owed to the state government. The company’s stockholders’ equity increased by the $1,000 generated by management (sales).

The asset and liability method places emphasis on the valuation of current and deferred tax assets and liabilities. The amount of income tax expense recognized for a period is the amount of income taxes currently payable or refundable, plus or minus the change in aggregate deferred tax assets and liabilities. Under this method, which focuses on the balance sheet, the amount of deferred income tax expense is determined by changes to deferred tax assets and liabilities. Based on the above calculations, the Lowell Merchandising Corporation would report income taxes expense of $1,400,000 on its income statement.

For example, as discussed in Chapter 9, a company might use straight-line depreciation in its accounting system and accelerated depreciation for tax purposes. The company’s resources do not change because the taxes will be paid according to government tax payment schedules. Its liabilities increase because the company owes the government $1,400,000.

How Do Accounts Payable Show on the Balance Sheet?

The situation is further complicated by the fact that the accounting methods used for tax purposes may differ from the methods used in the preparation of financial statements. Remember FIFO and LIFO inventory methods from Chapter 8 and straight-line and accelerated depreciation from Chapter 9? In general, for tax purposes, income taxes to governments are determined according to governmental tax rules, while for financial statement purposes, income taxes are based on taxable income.