Cash Flow From Financing Activities Example and Explanation

A business’s reported investing activities give insights into the total investment gains and losses it experienced during a defined period. Investing activities are a crucial component of a company’s cash flow statement, which reports the cash that’s earned and spent over a certain period of time.

Which is an example of a cash flow from a financing activity?

Cash flow from financing activities (CFF) is a section of a company’s cash flow statement, which shows the net flows of cash that are used to fund the company. Financing activities include transactions involving debt, equity, and dividends.

If a company buys a piece of machinery, the cash flow statement would reflect this activity as a cash outflow from investing activities because it used cash. If the company decided to sell off some investments from an investment portfolio, the proceeds from the sales would show up as a cash inflow from investing activities because it provided cash. In the statement of cash flows, the cash flow from these activities is listed in the operating activities section. They are focused changes in the current assets and current liabilities and the net income. Apart from operating activities, cash flow statement also lists the cash flow from investing and financing activities.

To summarize other linkages between a firm’s balance sheet and cash flow from financing activities, changes in long-term debt can be found on the balance sheet, as well as notes to the financial statements. Dividends paid can be calculated from taking the beginning balance of retained earnings from the balance sheet, adding net income, and subtracting out the ending value of retained earnings on the balance sheet. This equals dividends paid during the year, which is found on the cash flow statement under financing activities. A company’s CFF activities refer to the cash inflows and outflows resulting from the issuance of debt, the issuance of equity, dividend payments and the repurchase of existing stock. A firm’s cash flow from financing activities relates to how it works with the capital markets and investors.

This information shows both companies generated significant amounts of cash from daily operating activities; $4,600,000,000 for The Home Depot and $3,900,000,000 for Lowe’s. It is interesting to note both companies spent significant amounts of cash to acquire property and equipment and long-term investments as reflected in the negative investing activities amounts. For both companies, a significant amount of cash outflows from financing activities were for the repurchase of common stock. Apparently, both companies chose to return cash to owners by repurchasing stock.

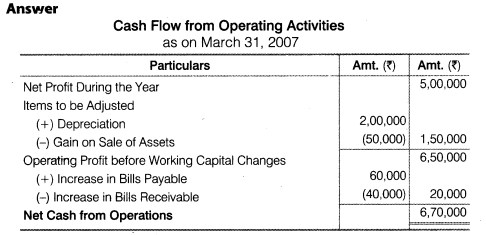

This report shows the net flow of funds used to run the company including debt, equity, and dividends. The cash flow from operating activities section shows a company’s cash flows from its core business operations, which it uses to reinvest in and grow its business. A healthy business should generate positive net cash flow from operating activities and should grow the amount over time.

Increasing debt causes leverage ratios such as debt-to-equity and debt-to-total capital to rise. Debt financing often comes with covenants, meaning that a firm must meet certain interest coverage and debt-level requirements. In the event of a company’s liquidation, debt holders are senior to equity holders. In the cash flow statement, financing activities refer to the flow of cash between a business and its owners and creditors. It focuses on how the business raises capital and pays back its investors.

Investing activities include cash activities related to noncurrent assets. Financing activities include cash activities related to noncurrent liabilities and owners’ equity. The largest line items in the cash flow from financing section are dividends paid, repurchase of common stock and proceeds from issuance of debt. Dividends paid and repurchase of common stock are uses of cash, and proceeds from the issuance of debt are a source of cash.

Through this section of a cash flow statement, one can learn how often (and in what amounts) a company raises capital from debt and equity sources, as well as how it pays off these items over time. Investors are interested in understanding where a company’s cash is coming from. If it’s coming from normal business operations, that’s a sign of a good investment. If the company is consistently issuing new stock or taking out debt, it might be an unattractive investment opportunity.

Transactions That Cause Positive Cash Flow From Financing Activities

Debt financing includes principal, which must be repaid to lenders or bondholders, and interest. While debt does not dilute ownership, interest payments on debt reduce net income and cash flow. This reduction in net income also represents a tax benefit through the lower taxable income.

Cash flow from operating activities excludes money that is spent on capital expenditures, cash directed to long-term investments and any cash received from the sale of long-term assets. Also excluded are the amounts paid out as dividends to stockholders, amounts received through the issuance of bonds and stock and money used to redeem bonds. It’s important for accountants, financial analysts, and investors to understand what makes up this section of the cash flow statement and what financing activities include. Since this is the section of the statement of cash flows that indicates how a company funds its operations, it generally includes changes in all accounts related to debt and equity.

A positive number for cash flow from financing activities means more money is flowing into the company than flowing out, which increases the company’s assets. Cash flow from financing activities provides investors with insight into a company’s financial strength and how well a company’s capital structure is managed. Operating cash flow is just one component of a company’s cash flow story, but it is also one of the most valuable measures of strength, profitability, and the long-term future outlook.

That’s especially true in capital-driven industries like manufacturing, which require big investments in fixed assets to grow their businesses. The first part of a cash flow statement analyzes a company’s cash flow from net income or losses. For most companies, this section of the cash flow statement reconciles the net income (as shown on the income statement) to the actual cash the company received from or used in its operating activities. To do this, it adjusts net income for any non-cash items (such as adding back depreciation expenses) and adjusts for any cash that was used or provided by other operating assets and liabilities.

- The cash flow from the financing activities section shows cash flows from issuing and paying off outside financing, such as stock and debt, and from paying dividends.

As a mature company, Apple decided that shareholder value was maximized if cash on hand was returned to shareholders rather than used to retire debt or fund growth initiatives. The financing activity in the cash flow statement focuses on how a firm raises capital and pays it back to investors through the capital markets. These activities also include paying cash dividends, adding or changing loans, or issuing and selling more stock. This section of the statement of cash flows measures the flow of cash between a firm and its owners and creditors. Cash flow from financing activities (CFF) measures the movement of cash between a firm and its owners, investors, and creditors.

If a business fails to consistently generate positive net cash from operating activities, it may need to rely on outside financing to operate, which will not sustain a business long term. Cash flow from investing activities is a line item on a business’s cash flow statement, which is one of the major financial statements that companies prepare. Cash flow from investing activities is the net change in a company’s investment gains or losses during the reporting period, as well as the change resulting from any purchase or sale of fixed assets. Financing activities primarily involve stockholder’s equity or owner’s equity, long-term liabilities, and the alterations that occur to short- term liabilities. The financing activities are often reported in a distinct segment of the financial statement referred to as the cash flow statement or the statement of cash flows, (SCF).

The cash flow from the financing activities section shows cash flows from issuing and paying off outside financing, such as stock and debt, and from paying dividends. A negative amount suggests the business is using its cash flow from operating activities to pay dividends and pay off its outside financing. The cash flow from financing activities are the funds that the business took in or paid to finance its activities. It’s one of the three sections on a company’s statement of cash flows, the other two being operating and investing activities.

A company that frequently turns to new debt or equity for cash might show positive cash flow from financing activities. However, it might be a sign that the company is not generating enough earnings. It is important that investors dig deeper into the numbers because a positive cash flow might not be a good thing for a company already saddled with a large amount of debt. If a company reports a negative amount of cash flow from investing activities, that’s a good clue that the business is investing in capital assets, which means in the future, you can expect their earnings to grow.

Cash Flow From Financing Activities – CFF

The financing activities of a business provide insights into the business’ financial health and its goals. A positive cash flows from financing activities may show the business’ intentions of expansion and growth. With more money is flowing in than flowing out, a positive amount indicates an increase in business assets.

A positive number on the cash flow statement indicates that the business has received cash. On the other hand, a negative figure indicates the business has paid out capital such as making a dividend payment to shareholders or paying off long-term debt.

We can see that the majority of Walmart’s cash outflows were due to the purchase of company stock for $8.298 billion, dividends paid for $6.216 billion, and payments of long-term debt of $2.055 billion. Although the net cash flow total is negative for the period, the transactions would be viewed as positive by investors and the market. Any significant changes in cash flow from financing activities should prompt investors to investigate the transactions. When analyzing a company’s cash flow statement, it is important to consider each of the various sections that contribute to the overall change in its cash position.

Examples of Financing Activities comprising the owner’s equity involve the issuance of preferred or common stock. Escalation in these stock accounts is stated as positive totals in the financing activities segment of the cash flow statement. The positive sums connote that cash was offered by issuing more shares of stock which is a source of cash. If a firm raises funds through debt financing, there is a positive item in the financing section of the cash flow statement as well as an increase in liabilities on the balance sheet.

How Do the Balance Sheet and Cash Flow Statement Differ?

It is derived either directly or indirectly and measures money flow in and out of a company over specific periods. Unlike net income, OCF excludes non-cash items like depreciation and amortization, which can misrepresent a company’s actual financial position. It is a good sign when a company has strong operating cash flows with more cash coming in than going out.

The activities include issuing and selling stock, paying cash dividends and adding loans. The company engaged in a number of financing activities during 2014 after announcing intentions to acquire other businesses. When a company raises funds through equity financing, there is a positive item in the cash flows from financing activities section and an increase of common stock at par value on the balance sheet. The three categories of cash flows are operating activities, investing activities, and financing activities.

Cash flow from financing activities (CFF) is a section of a company’s cash flow statement, which shows the net flows of cash that are used to fund the company. Financing activities include transactions involving debt, equity, and dividends. Investing activities are one of the main categories of net cash activities that businesses report on the cash flow statement. Investing activities in accounting refers to the purchase and sale of long-term assets and other business investments, within a specific reporting period.